Warsaw real estate prices increased by 57% in the last 5 years (source). Is it a bubble?

Chart source: Sonarhome

Most likely not - as the housing boom was driven by fundamental factors and not over-leveraging. Data used below measures changes between Jan 1 2020 to Jan 1 2025.

Wealth increase

- 15% GDP growth during period (surpassing Portugal in PPP per capita terms)

- 59% increase in average wages across the country and likely higher in Warsaw.

- Warsaw's purchasing power is now 6% above EU average

- Average wages increased at a higher rate vs real estate prices, Measured in local income terms - real estate became more affordable

Population increase

- 13% increase in Warsaw’s population

- Urbanization - Poles from smaller cities moving to the capital city

- Return migration - Poles from countries like the UK moving back

- New migrants - primarily from Ukraine and Belarus, but increasingly from other countries as well

Government backed mortgages

- During the second part of 2023, the government briefly launched a government backed loan program. Eligible borrowers were able to obtain mortgage loans with rates at 2%.

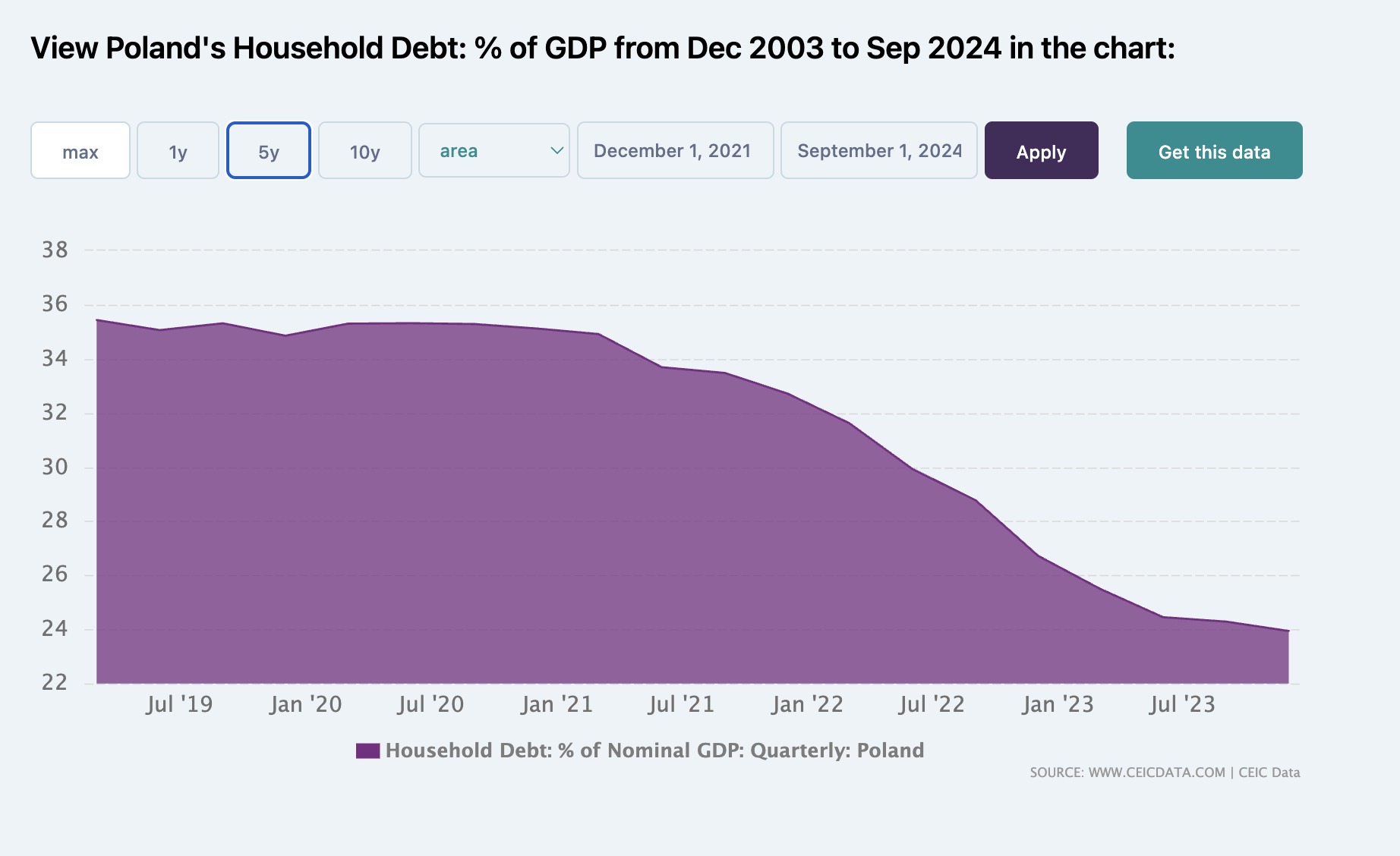

No signs of over leveraging and over valuation

- Poland is one of the least leveraged markets globally, with the majority of real estate transactions still taking place without mortgage loans.

- Low leverage means that Polish real estate prices are much less sensitive to global market and rate changes, offering investors a less correlated asset to global equities and developed market real estate.

- The above is proven by the fact that real estate prices grew at a time when mortgage rates spiked to 8%

- UBS ranks Warsaw as having the third lowest real estate bubble risk globally, out of the major international cities surveyed (Source: Global Real Estate Bubble Index 2024)

- Warsaw real estate is still priced 30% below Prague, Czech Republic. This is despite the average spending power of locals in Warsaw being stronger (€19,878 in Warsaw vs €18,667 in Prague).

- Foreigner buyers make up less than 6% of total Polish real estate transactions in 2023 - much lower than Portugal (12%) and Spain (15%) - thus better insulating Warsaw real estate prices from external factors.

The content and links are confidential and intended for the recipient only. It shall not be shared in full or in part, with any third party, without the written consent of Jason Wong. None of the content shall be construed as legal, tax, investment or financial advice. Nor should you rely on the content to make any decisions, financial or otherwise.

Driving factors for further increase in real estate prices

1. Continued population growth and economic growth

- Continued population increase from return migration of Poles in the West, as well as external migrants (both EU and non EU)

- Continued economic and salary growth above the EU and US average (see table below)

- More insulated from US tariffs than the rest of the EU (Source: ING bank) with only 3.3% of Polish exports going to the US

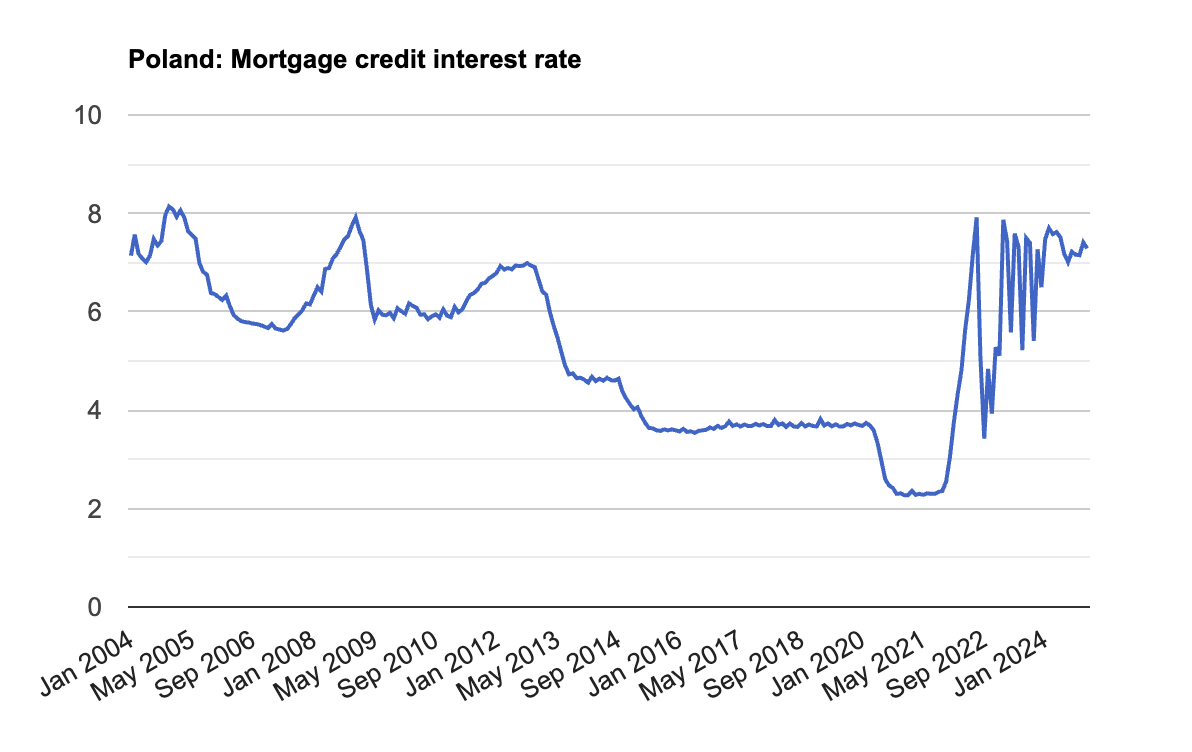

- Real estate continuing to act as the preferred investment vehicle of most Poles, thus capturing the country’s wealth increase (see chart below)

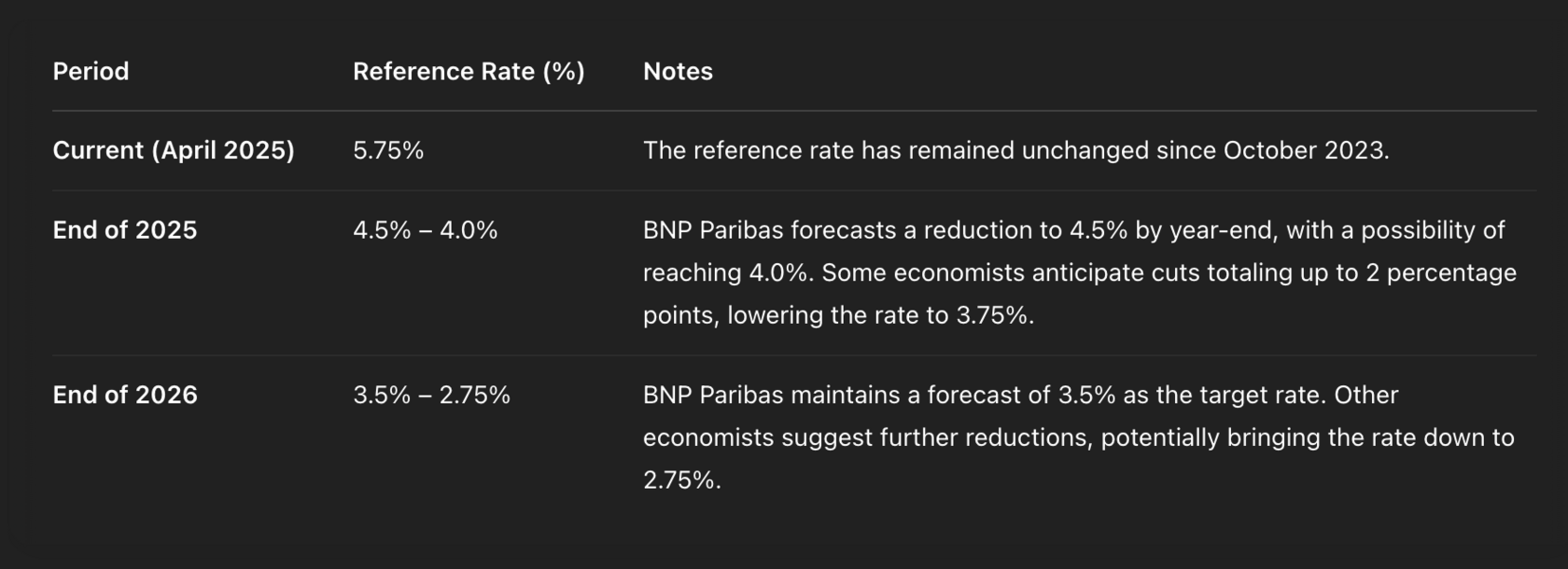

2. Significant rate cuts and possible government subsidies

- The government is working on new subsidized loans program designed to subsidize housing purchases for young people and families.

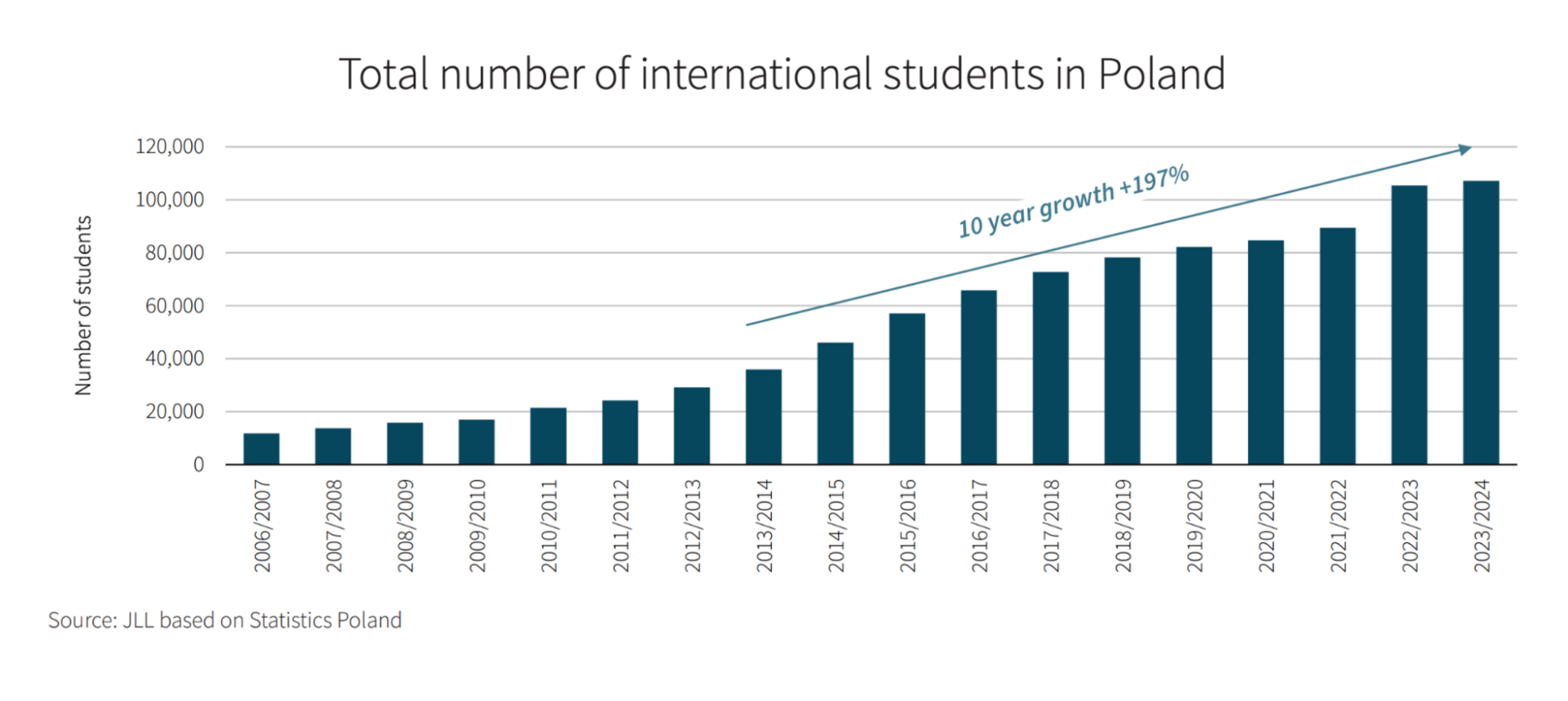

3. Fundamental housing shortage

- Looking specifically at the student housing segment in Warsaw, there is a deficit of 60,000 beds (Source: JLL) supported by the continuous increase of international students - many of whom stay in Poland post graduation.

- This especially opens up room for investors looking to rent to university students and young professionals at the start of their career.

De-dollarization hedge

- If you are a USD denominated investor looking for an asset not correlated with the USD, the Polish Zloty (PLN) trades closely with EUR - thus allows you to track EUR’s upside, whilst earning a higher yield. (Purple line: USD/EUR, Blue line: USD/PLN since 2004)

- During times of extreme USD weakness, such as the 2008 financial crisis - the Polish Zloty traded 46% stronger than USD. Therefore Polish Zloty denominated real estate offers a USD denominated investor significant upside in the event of a continuous decrease in USD value.

Summary

- The exceptional price growth in the last 5 years was driven by fundamental factors. Measured in terms of local purchasing power - real estate in Warsaw became cheaper, not more expensive.

- If you believe in the Polish growth story continuing, real estate in the capital city remains a good investment vehicle to capture this growth. This is supported by fundamentals such as Warsaw’s population growth, housing deficit and interest rate cuts.

- Assuming an annual appreciation of 5%, it would still take 5 years of compounded increases for Warsaw’s median real estate price to reach Prague’s current prices (despite Warsaw being wealthier in purchasing power terms).

- Targeting 5% appreciation + 5% net rental yield appears realistic over the next 5 years (28% compounded total appreciation). Real estate can also be sold free of any capital gains tax in Poland after 5 years.

Flag Ventures helps you remotely access undervalued real estate and fixed income investments globally. We focus on lesser known opportunities, especially those in emerging markets.

This report was originally published in May 2025.